Guidelines for payment for services in the UK or overseas

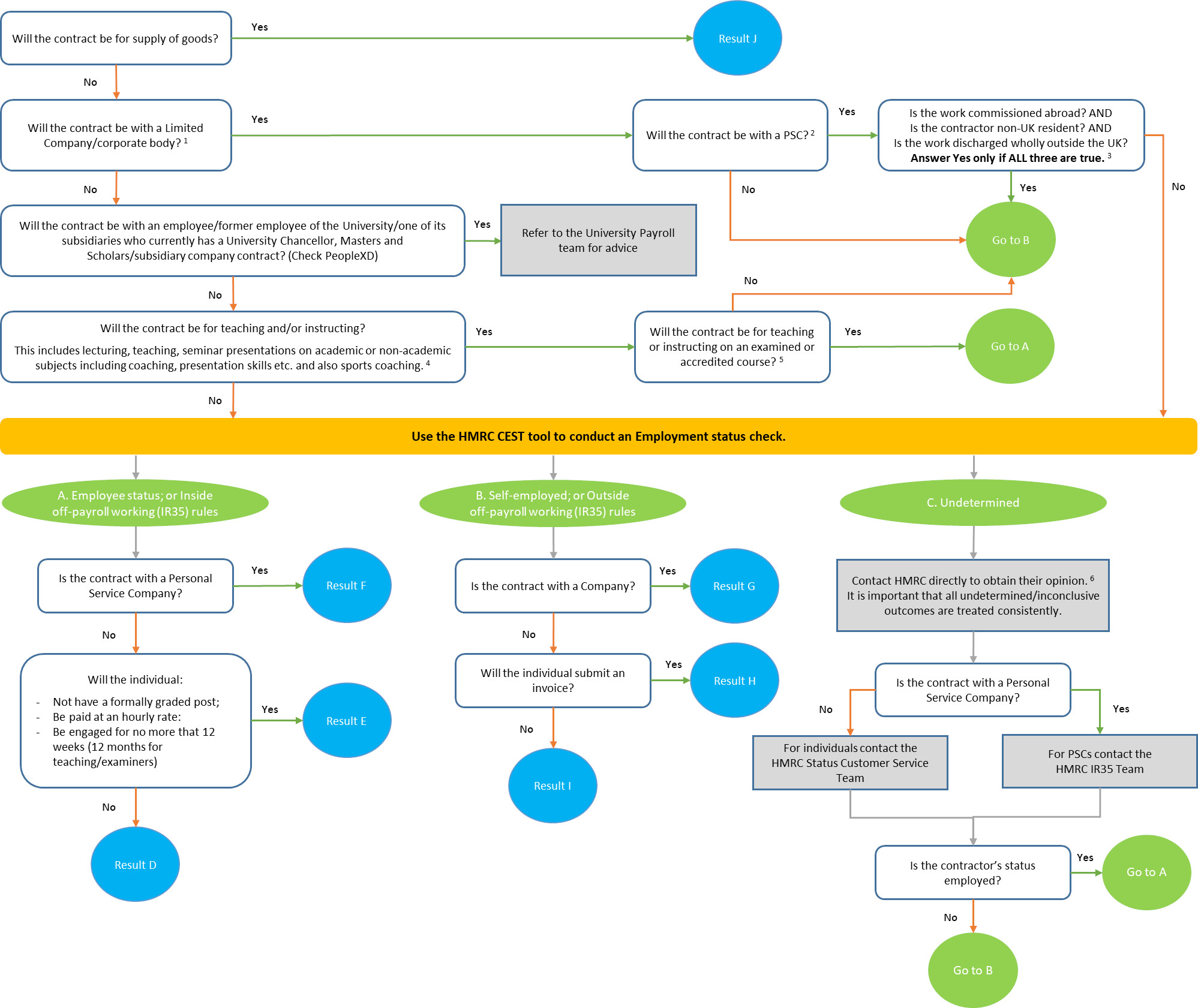

Flowchart to determine the correct engagement and payment route for provision of services

A printable checklist (docx) of this flowchart is available to complete and submit with any request for payment.

| Result | Payment process | Tax treatment | Next steps and how to pay |

|---|---|---|---|

| Payroll process | Tax and NI deducted |

|

|

| Payroll process | Tax and NI deducted |

|

|

| Payroll process | Tax and NI deducted |

|

|

| Accounts payable process | Do not deduct tax or NI |

|

|

| Accounts payable process | Do not deduct tax or NI |

|

|

| Accounts payable process | Do not deduct tax or NI |

|

|

| J - Supply of goods | Accounts payable process | Do not deduct tax or NI |

|

Notes:

1. Limited Company or other corporate body invoices must contain the company name and be for payment to a company bank account. Ideally the invoice will also include a company registration number and/or VAT registration number. All UK incorporated companies should be registered at Companies House. If you are in any doubt process the invoice as if it comes from an individual.

2. The generally accepted definition of a Personal Service Company (PSC) is a limited company typically with a sole director, the contractor, who owns most/all of the shares. The contractor’s PSC generally supplies professional services to end user clients, either directly or via an agency. The services are delivered by the contractor who is also the owner and director of the business. All UK company directors should be registered at Companies House.

3. Contractors hired through a foreign PSC may be affected by the off-payroll working (IR35) rules (formerly the intermediaries’ legislation). There may also be fiscal implications abroad for which we invite administrators to contact the Payroll Manager.

4. A part-time lecturer whose engagement covers a complete academic term or longer may well have similar terms and conditions to a full-time lecturer. Many such part-time lecturers will be employees. A visiting lecturer who gives an occasional talk or short series of talks on a subject about which she/he has specialist knowledge and which is not part of the core curriculum will normally have rather different terms and conditions and is likely to be self-employed. Engagements should be considered on their own facts and the CEST tool must be completed to determine status.

5. Examined and Accredited courses do not include those that only issue a certificate of attendance or similar.

6. If the result relates to a visiting lecturer/trainer, please refer to our website for more information.

7. All payments to an individual processed through the Accounts Payable process will be recorded, where applicable, for declaration to HMRC in accordance with HMRC regulations.